Service tax

Published: 2018

Effective Date and Scope of Taxation

1 September 2018 (Service Tax)

- Service tax is a consumption tax levied and charged on any taxable services provided in Malaysia by a registered person in carrying on his business.

1 January 2019 (Imported Service Tax)

- Service tax is also charged on the importation of taxable service acquired by any person who carries on business in Malaysia.

1 January 2020 (Digital Service by Foreign Service Provider)

- Service providers outside Malaysia who provide digital services to Malaysian consumers will be required to register in Malaysia and charge service tax.

Rate of Tax

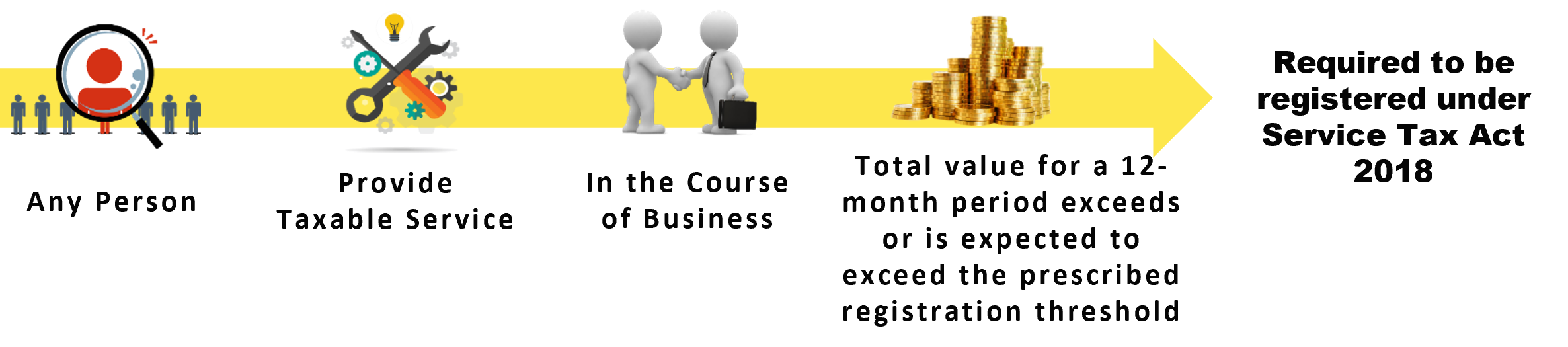

Registration of Taxable Person

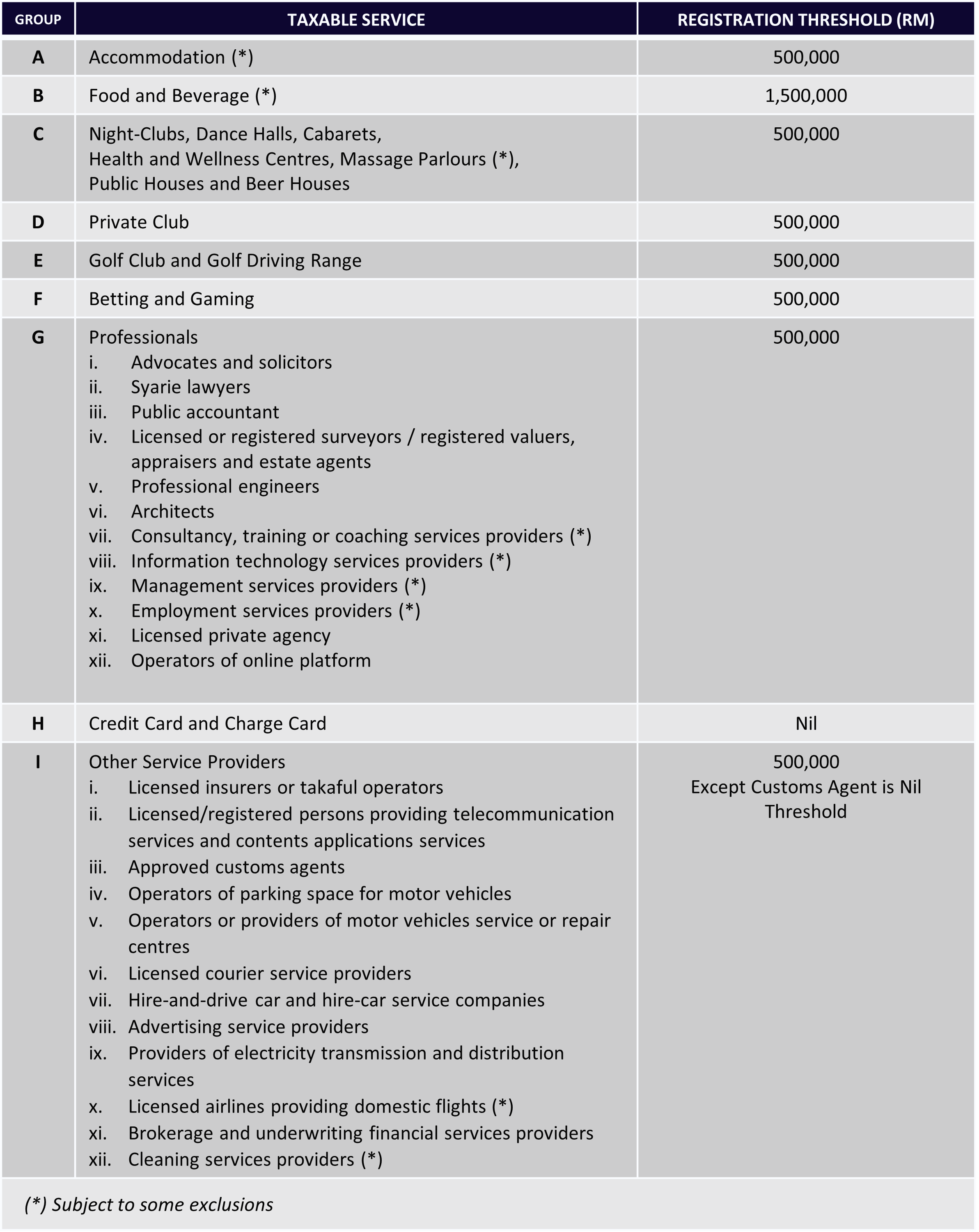

Taxable Services

Payment of Service Tax and Taxable Period

1. Taxable Period

- A taxable period is a period of 2 calendar months, however, a taxable person can apply to the DG of Customs to vary the taxable period.

- The return shall be furnished to the Director General not later than the last day of the month following the end of his taxable period using form SST-02.

2. Service Tax Due

A. Payment received within 12 months from the date of invoice

- Service tax is due when payment is received for the taxable services rendered.

B. Payment is not received within 12 months from the date of invoice

- Where payment for any taxable service provided is not received within a period of 12 months from the date the taxable service was provided, Service Tax shall be due on the day following that period of 12 months.

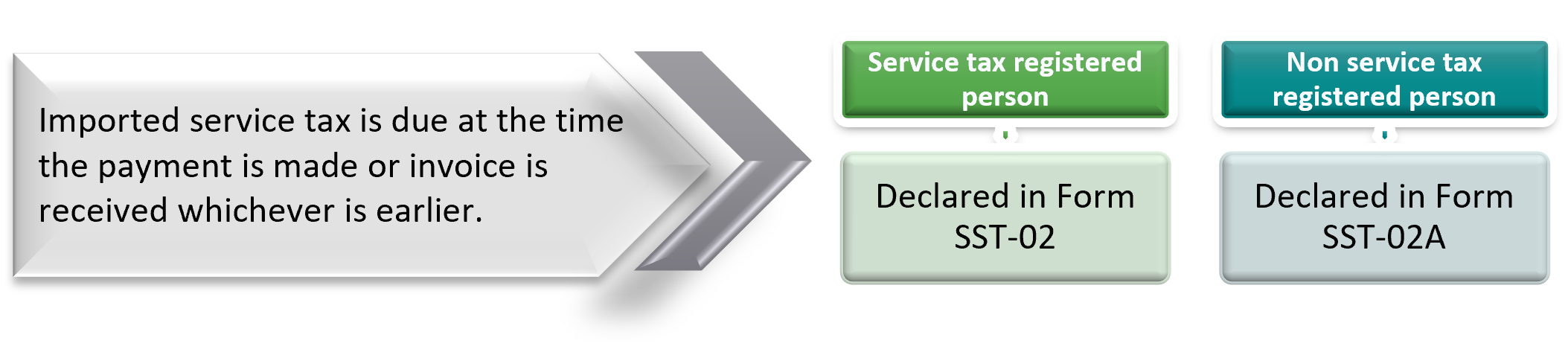

C. Imported taxable services

Offences & Penalties

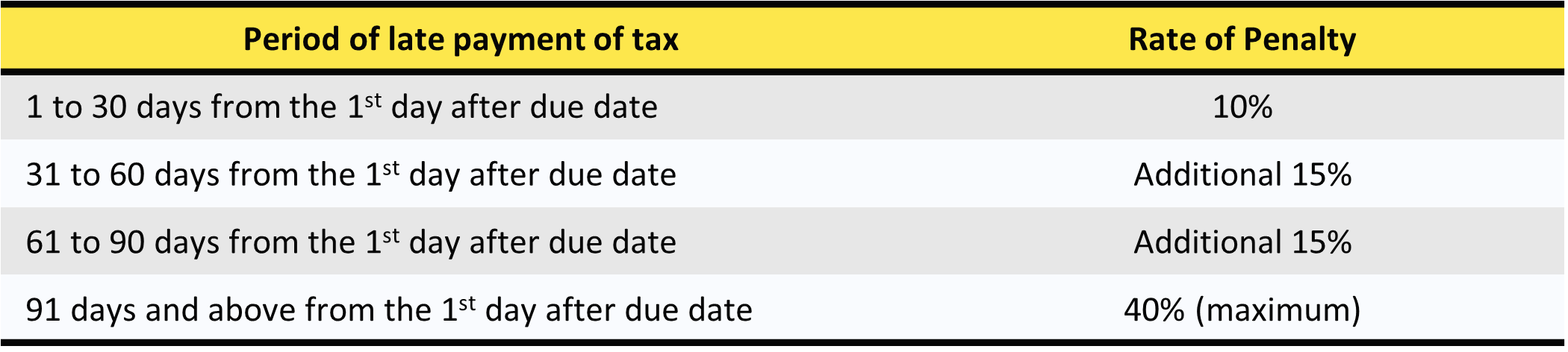

1. Late Payment Penalty

2. Evasion of Service Tax

Any person who, with intent to evade or to assist any other person to evade service tax:-

- Omits any information that affect the amount of service tax chargeable

- Makes any false statement or entry in any return, claim or application

- Give false answer

- False invoices or other false records

- Makes, uses or authorizes the use of any fraud, artifice or contrivance

First Offence

Fine not less than 10 times and not more than 20 times of the amount of service tax / imprisonment not exceeding 5 years, or both

Second and Subsequent Offence

Fine not less than 20 times and not more than 40 times of the amount of service tax / imprisonment not exceeding 7 years, or both

Table 1

Taxable Services Under First Schedule of Service Tax Regulations 2018

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.