The differences you must know in the Tax Treatments between a Resident and Non-Resident Company!

"Resident" means resident in Malaysia for the basis year for a year of assessment (YA) by virtue of section 8 and subsection 61(3) of the ITA.

"Non-Resident" means other than a resident in Malaysia by virtue of section 8 and subsection 61(3) of the ITA.

Determination of Residence Status of Companies

Management and control is the key factor used to ascertain the residence status of a company in Malaysia.

❑ The management and control refers to the controlling authority which determines the policies to be followed by the company.

❑ The management and control is considered to be exercised where the directors meet to conduct the company’s business / affairs irrespective of where the company might be incorporated.

❑ The management and control of a business of a company would depend upon how the business is managed.

❑ The location of the trading activities or the place of physical operations may not necessarily be the place of management and control.

❑ The appointment of a local director or local board of directors in Malaysia does not determine the residence status of a company.

❑ Control by the shareholders is not relevant for the determination of the management and control as share-holders exercise their power over the company by virtue of their voting power at formal meetings of shareholders

❑ The residence status of a director does not determine the residence status of a company.

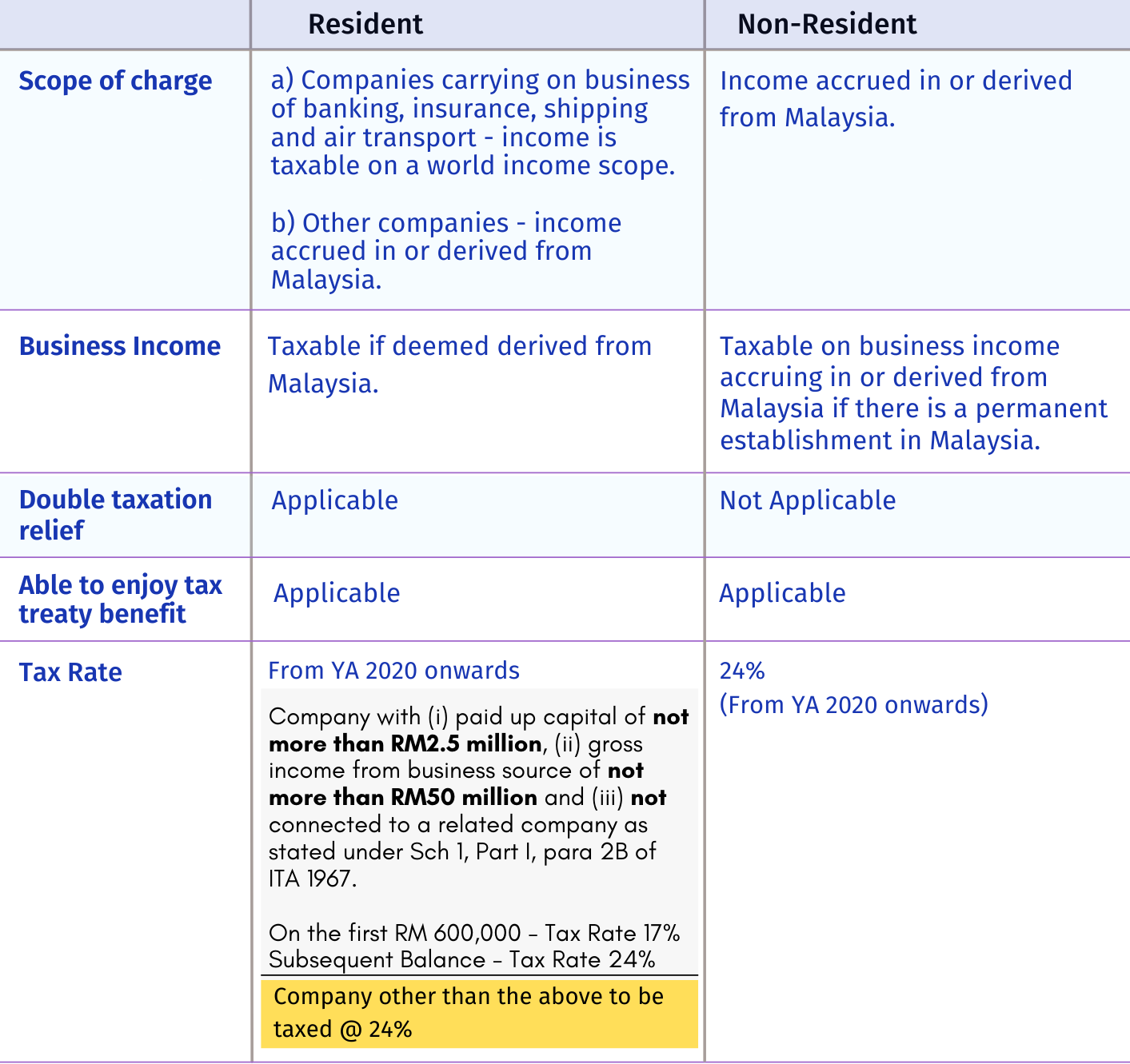

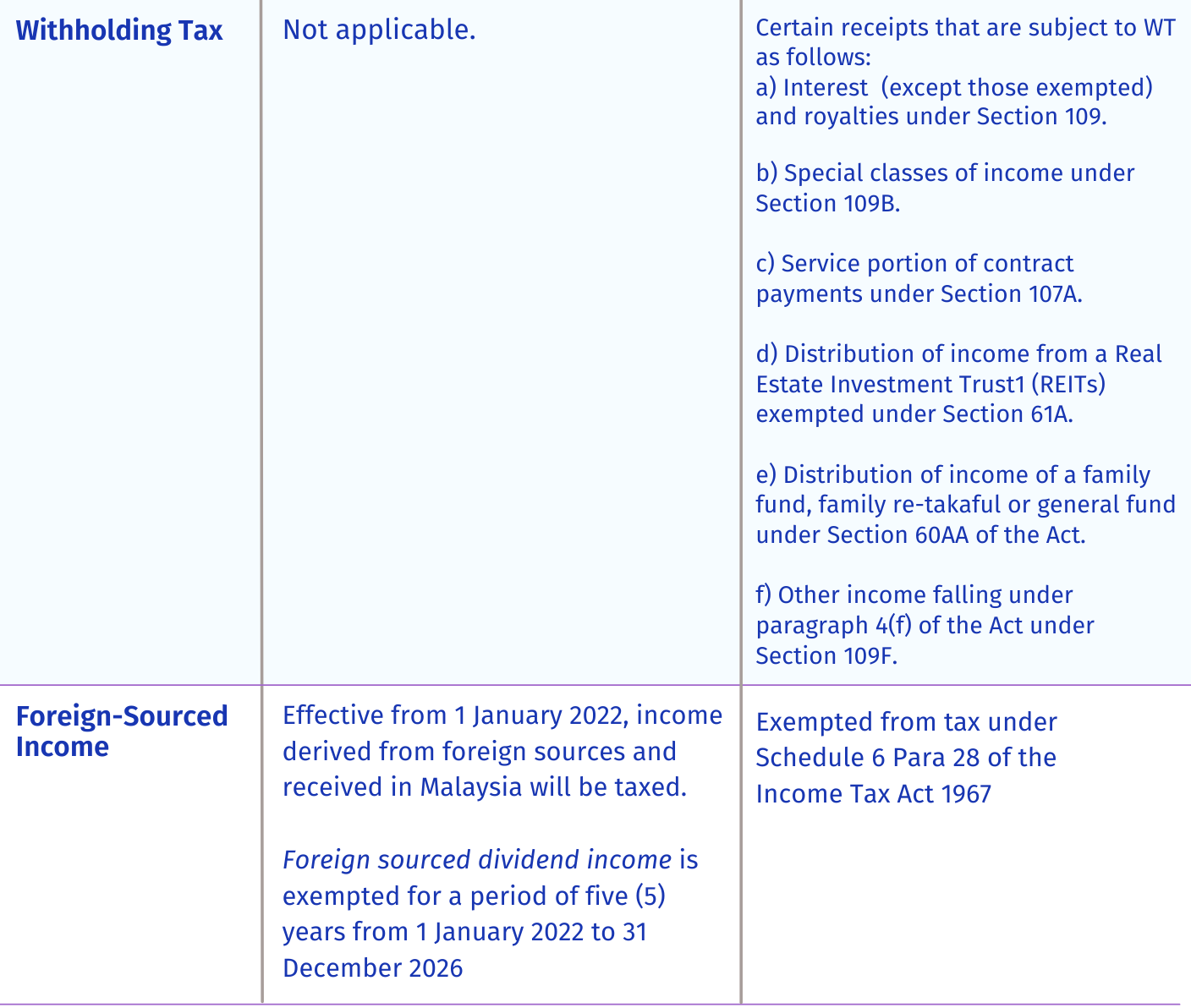

Differences in the Tax Treatments between a

"Resident" and "Non-Resident" Company

Reference: RESIDENCE STATUS OF COMPANIES AND BODIES OF PERSONS Public Ruling No. 09/2019

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.