Tax Treatment on Sums Received and Debts Owing for Services to be Rendered

Public Ruling No 4/2020

Published: 2021

Background

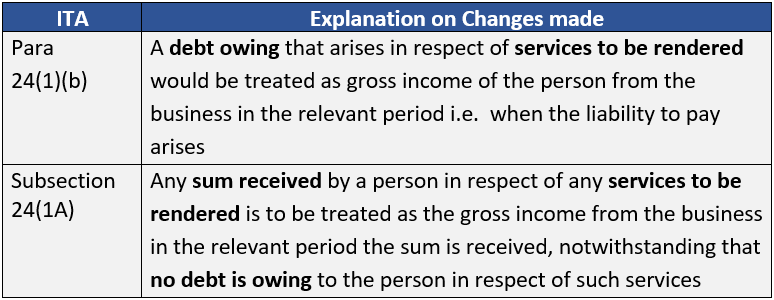

Prior to the year of assessment (YA) 2016, paragraph 24(1)(b) of the ITA only dealt with debts arising in respect of any services rendered which were treated as gross income in the YA the debt arises. In other words, advance payments received was treated as gross income from a business when the service is rendered.

With effect from YA 2016, paragraph 24(1)(b) has been revised and a new subsection 24(1A) has been inserted to deal with debts arising and sums received in the course of business in respect of services to be rendered.

Briefly, the changes are as below.

Public Ruling 4/2020

The IRBM has issued PR 4/2020 - Tax Treatment of Any Sum Received and a Debt Owing that Arises in Respect of Services to be Rendered dated 16 June 2020 to explain the tax treatment relating to the above changes.

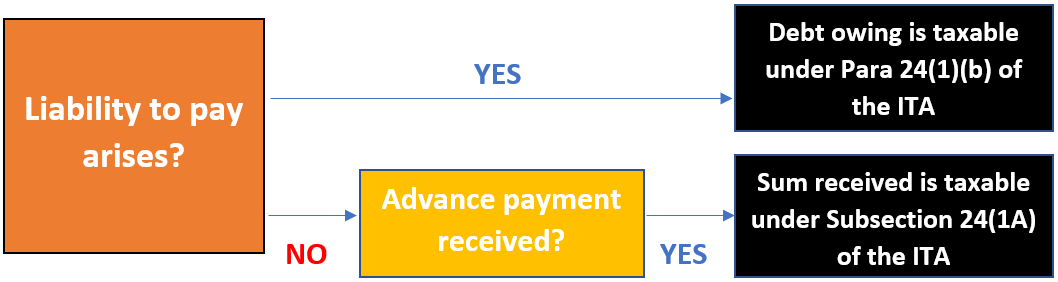

Application of paragraph 24(1)(b) of the ITA and subsection 24(1A) of the ITA

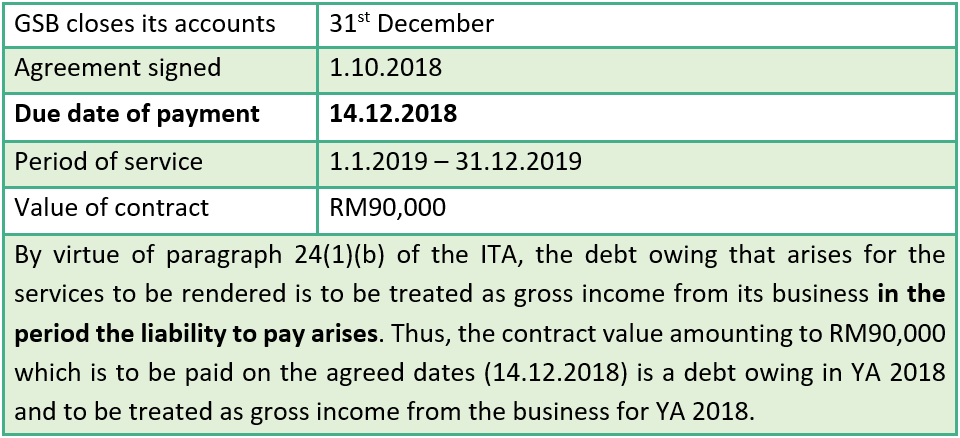

Example A:

Galaxy Sdn Bhd (GSB) provides office cleaning services. On 1.10.2018, an agreement was signed with a regular client, Lavender Sdn Bhd (LSB). The summary of the agreement between GSB and LSB is as below:

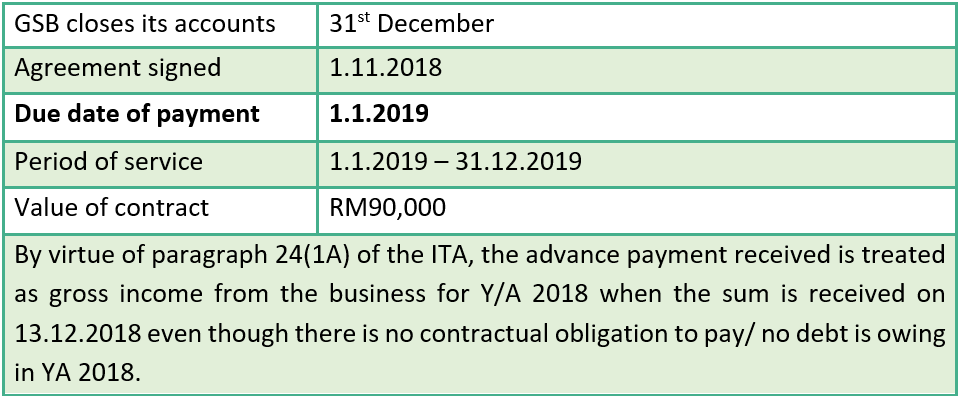

Example B:

Same facts as in Example A except that on 13.12.2018, LSB made an advance payment of RM90,000 which was supposed to be due and payable on 1.1.2019.

Tax Treatment in Respect of a Refund of an Advanced Payment

Pursuant to subsection 34(7A) of the ITA, if a person refunds any sum of money received in respect of services that have yet to be rendered, a tax deduction can be claimed in the YA when the refund is made.

Services that are Not Subject to Paragraph 24(1)(b) and Subsection 24(1A) of the ITA

The following are services not subject to the above tax treatment:

- Services that are governed by separate Income Tax Rules – i.e., services provided under a construction contract or property development.

- Pursuant to Subsection 24(8) of the ITA, Section 24 of the ITA shall no apply to income under Section 4A of the ITA which is in relation to services provided by a non-resident person.

- Deposits for any service received by a service provider upon the signing of an agreement where the deposits are refundable upon completion of the service, do not form part of the gross income of the service provider’s business under section 24 of the ITA – i.e., security deposit and refundable deposit.Deposits that are forfeitable if the terms and conditions of the agreement are not adhered to.

- Deposits that are subsequently forfeited (not refunded) would be part of the gross income of the service provider’s business under the provisions of paragraph 4(a) of the ITA.

To Grow a Business You Need EQUITY PLANNING 7.0

Will you be able to conquer the market and grow your business even at this critical period?

It’s all in your hands whether you decide to join this seminar of the year which allow you to create unlimited possibilities for your enterprise!

Get guidance from our most professional and practical coaches, learn everything you must know about equity planning, valuation, inheritance and listing altogether in this seminar.

Register NOW and make your winning move towards growing your business to greater heights!

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.