Published: 2021

General Principle

Generally, the compensation for loss of employment received by an employee is subject to tax under Section 13(1)(e) of the ITA 1967 as follows:

Section 13 - Employment income

Gross income of an employee in respect of gains or profits from an employment includes —

1(a): Monetary Benefit

1(b): Benefits in Kind

1(c): Enjoyment via living accommodation in Malaysia

1(d): Contributions made by employer to an unapproved pension or provident fund

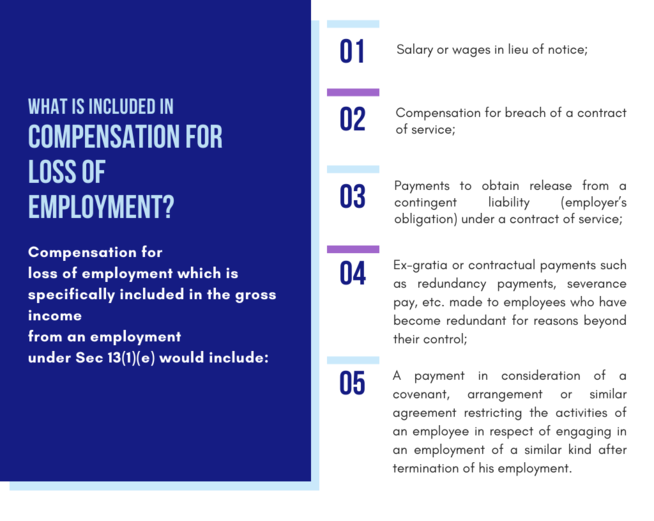

1(e): Amount paid to an employee (whether before or after his employment ceases) as compensation for loss of the employment

Section 13(1)(e)

Determination of Elements of Compensation and Gratuity

It

is essential to determine whether the payment made to employee is in the nature

of gratuity or compensation for loss of employment as different tax treatment

is accorded for gratuity payment. Please refer to our previous article for tax

treatment of gratuity received by an employee.

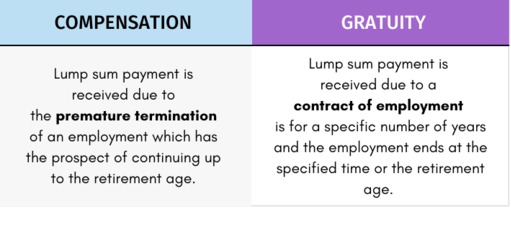

In general, the distinction between compensation for loss of employment

and gratuity is as follows:

Tax Treatment of Compensation for Loss of Employment

Exemption for Section 13(1)(e) - [Para 15 of Sch 6 of the ITA 1967]

Compensation for loss of employment (other than a payment by a controlled company to a director of the company who is not a full-time service director) is exempted from income tax in the following circumstances:

✓ Full exemption

If the Director General is satisfied that the payment is made on account of loss of employment due to ill-health (required to be certified by a Medical Board);

OR

✓ Partial exemption

An exemption of RM10,000 is given for each completed year of service with the same employer or with companies in the same group.

Attention:

The MOF has announced via the Finance Act 2020 that the income tax exemption

for compensation for loss of employment to be increased from RM10,000 to RM20,000

for each full year of service with the same employer or with companies within the same group

with effect from YA 2020 to 2021.

Separation Scheme

Effective

from YA 2007, compensation for the payment received by an employee from an

employer for an early termination of an employment contract (including

termination under a Voluntary Separation Scheme (VSS) or Mutual Separation

Scheme) will be granted a tax exemption pursuant to subparagraph 15(3) of

Schedule 6 of the Act.

However, if the separation scheme offers the employees reemployment with

the same employer or any other employer, the payment under the scheme does not

qualify for an exemption.

Reference: PR No. 1/2012

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.