YYC Newsletter 25/6/2020

View in Mandarin

Special Tax Deduction on Rental Reduction

A special tax deduction was introduced in the earlier Economic Stimulus Package for landlords who reduce at least 30% rental on business premises rented to SME tenants, for period of April 2020 to June 2020.

This special deduction has now been extended to 30th September 2020 as announced in the Short-Term Economic Recovery Plan (PENJANA).

The following are the related Frequently Asked Questions:

- Who is eligible?

- What is the eligible period?

- Minimum rental reduction

- Rent reduced at different rates each month

- Amount of special deduction

- Definition of SMEs

- Who is not considered as SME?

- Premise rented to related company

- What is meant by business premise?

- Rental not applicable for special deduction

- Rental received in advance

- Supporting documents

- Illustration

1. Who is eligible?

- All taxpayers (individual/ cooperative/ other business/ non business entities) who rent out business premises to qualified SMEs tenants;

- The rented premises must be used by the SME tenant for business purpose;

- Landlord must be taxpayer who is receiving rental income under Subsection 4 (a) and 4 (d) of Income Tax Act 1967.

2. When is the eligible period?

From April 2020 until 30 September 2020.

3. What is the minimum rental reduction for landlord to enjoy this special deduction?

The rental reduction must be at least 30% from the current monthly rental rate.

4. Is the landlord eligible if he reduces the rent at different rate each month but all rate exceeds 30%?

Yes, as long as the reduction rates are not less than 30% in each of the eligible months.

If in any of these eligible months, the rental reduction is less than 30%, then the company is not eligible to claim the special deduction for that particular month/months.

5. What is the special deduction amount?

The amount of special deduction is equivalent to the amount of monthly rental reduction offered by landlord to eligible SMEs tenants.

6. Definition of SMEs

- The definition of SME for this purpose follows the National SME definition.

For more information, please click here to refer to the SME Definition Guideline - SMEs that are eligible for this special tax deduction are registered SMEs and have obtained SME Status Certificate from SME Corp. Malaysia

- Any queries regarding eligibility or registration as an SME can be directed to SME Corp at SME Corp Malaysia at 1300-30-6000 or email to info@smecorp.gov.my

7. Who is not considered as SMEs?

- Public listed entities on the main board

- Subsidiaries of:

✔ Publicly listed companies on the main board

✔ Multinational corporations (MNCs)

✔ Government linked companies (GLCs)

✔ Syarikat Menteri Kewangan Diperbadankan (MKDs)

✔ State owned enterprises

8. Is a company qualified for this deduction if rents out premise to related company?

The company (landlord) is eligible for this special deduction if the related company (tenant) qualifies as SME.

9. What is meant by business premises for this special deduction?

- All premises used for business purpose (i.e office/workshop/ childcare/ warehouse/ rented lot/ bazaar/ booth /stall).

- Residential house used for both residential and business is NOT qualified for this special deduction.

10. Is this special deduction applicable for rental of machines/ parking spaces/ telecommunication towers?

No. This special deduction is only applicable to rental of business premises used for business purpose only.

11. The landlord has received rental payment for April until June 2020 earlier this year.

Can the landlord offers rental reduction and claim special deduction?

Yes. Landlord who has received rental payment in advance is still allow to offer rental reduction as long as all conditions are fulfilled.

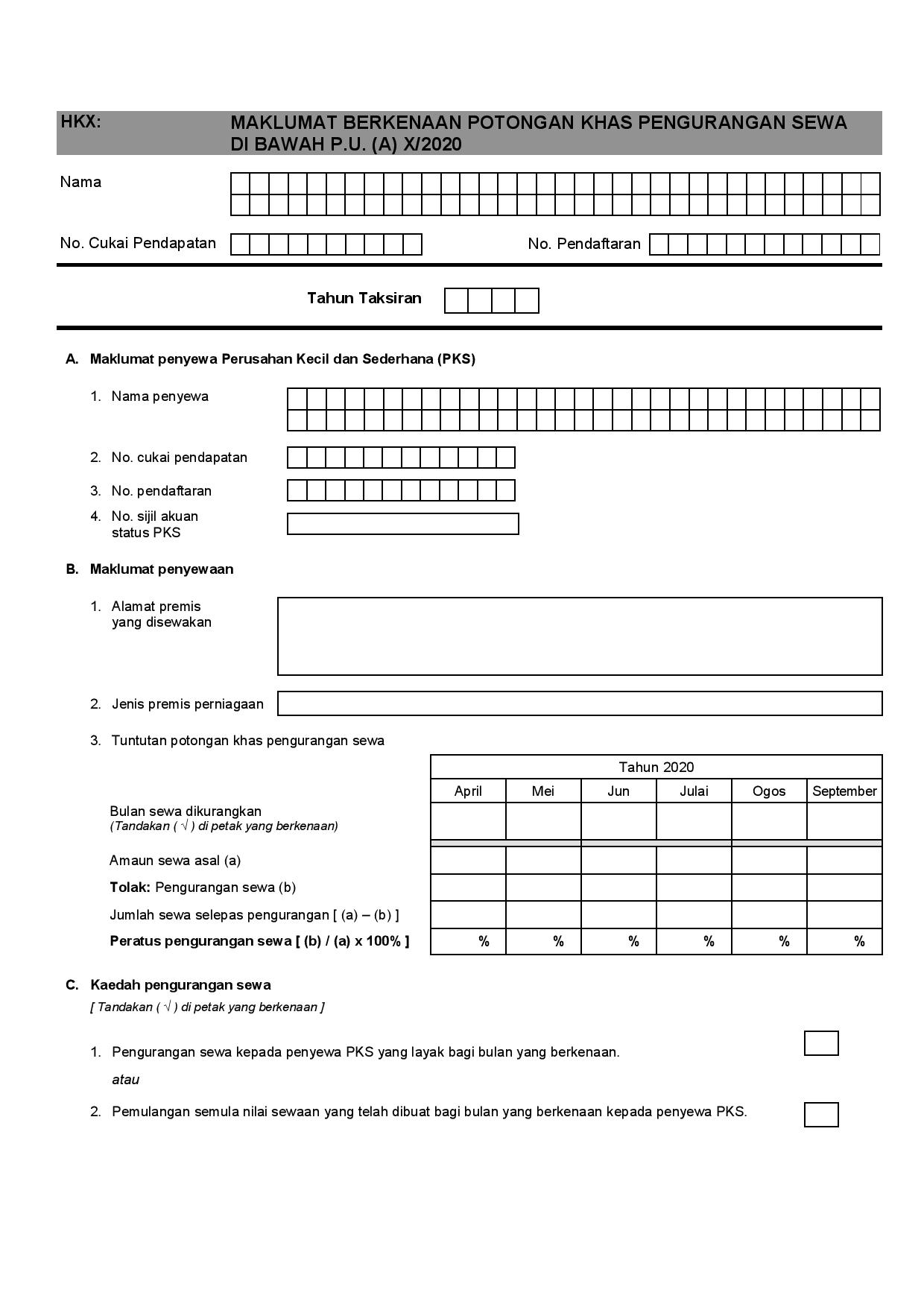

12. What are the required supporting documents?

Taxpayer (landlord) who claims this special deduction is required to keep the following documents:

i. Stamped tenancy agreement;

ii. Rental income statement;

iii. SME Status Certificate issued by SME Corp.*;

*Information regarding registration of SME can be referred at https://smereg.smecorp.gov.my

iv. Tenant’s information, rental information and rental reduction methods**

**To be provided in working sheet (HK) of Company Return Form, please refer to the example attached as below:

Click here to download the above sample working sheet

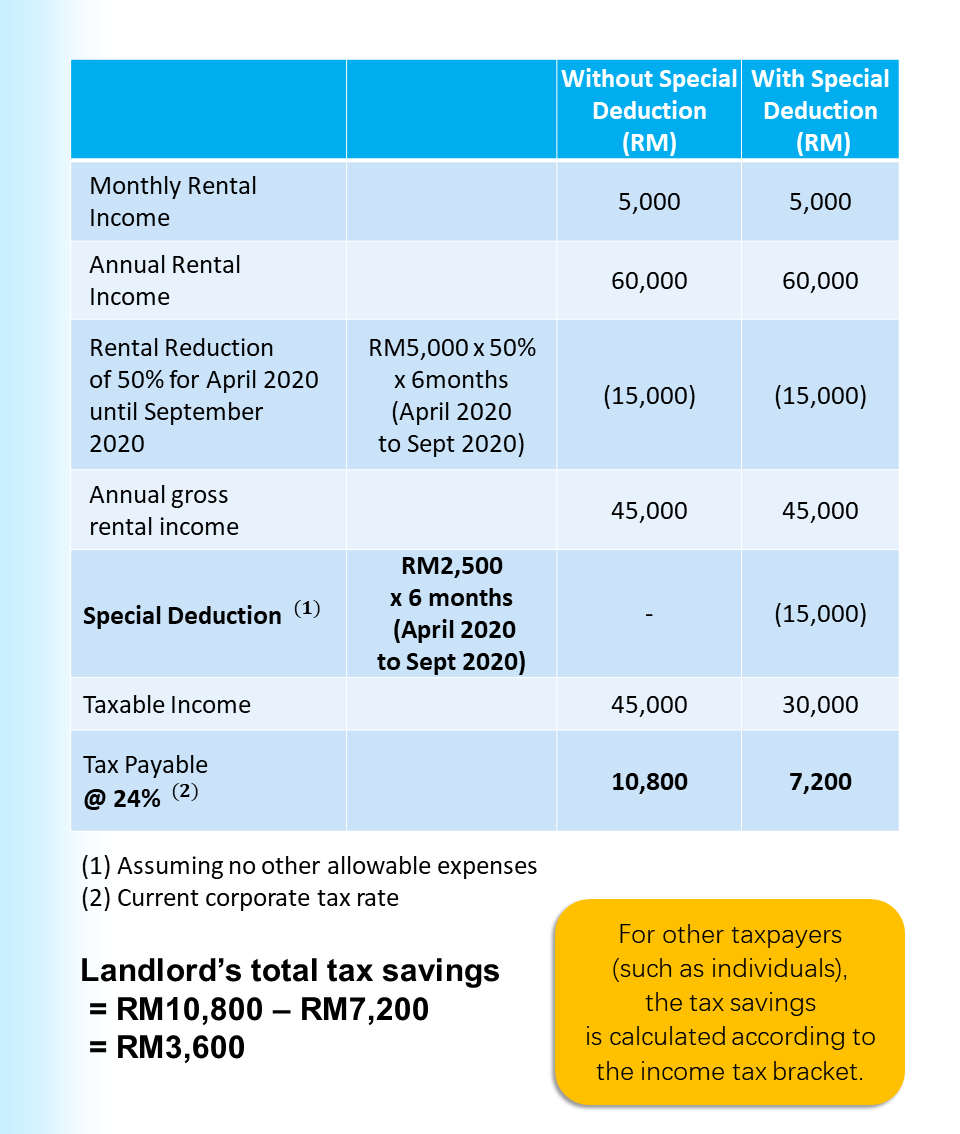

13. Illustration:

A Sdn Bhd rents a shop lot to B which is an eligible SME for RM5,000 a month (RM60,000 yearly).

A Sdn Bhd has agreed to offer rental reduction to B for the month of April 2020 to September 2020, of RM2,500 a month.

Source:

Rental Reduction for Business Premise by Inland Revenue Board of Malaysia (updated on 15 June 2020)

Generally, property buyers invest in real properties, such as houses, shops or factories under their personal name. However, some would choose to buy properties under the company's name.

What are the differences and the taxes involved? What will be the impact?

Find out in our upcoming Tax Property Webinar where we will cover:

- Is my income tax status suitable to buy property?

- How to calculate the stamp duty that I have to pay?

- How to report tax on income gained from property?

- Under what circumstances must I pay Real Property Gains Tax?

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.