Special Deduction on Business Premises: Renovation & Refurbishment

General Principle

The Government of Malaysia has initially introduced special tax deduction on cost of renovation incurred from 1 March 2020 to 31 December 2020 in the first economic stimulus package and subsequently this initiative has further extended until 31 December 2021.

To legislate the proposal, the Income Tax (Costs of Renovation and Refurbishment of Business Premise) Rules 2020 [P.U.(A) 381] was gazetted on 28 December 2020. Thereafter, the IRBM has published a Frequently Asked Questions (FAQs) to provide further clarification on the application of the rules.

Some of the key points are outlined as below:

Special deduction up to RM300,000 *Details are in P.U.(A) 381

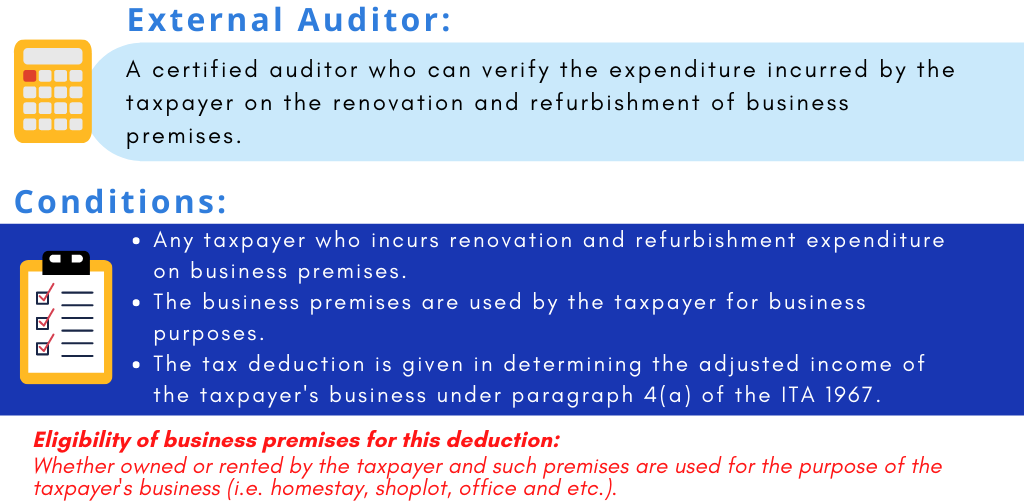

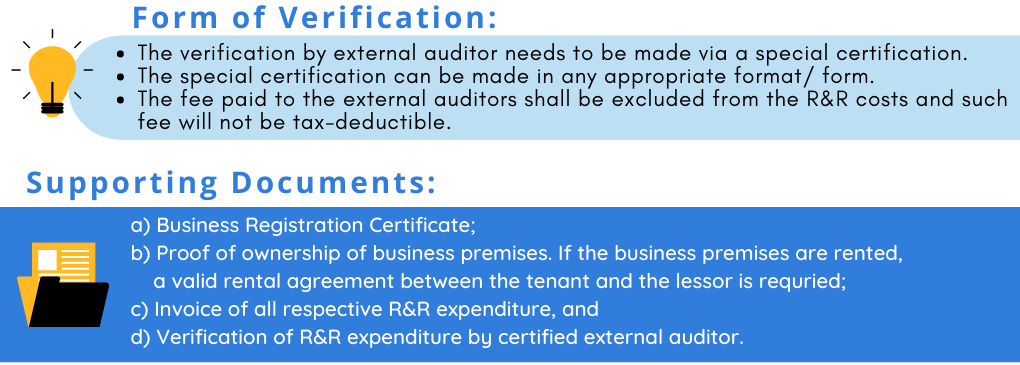

Allowed on the cost incurred for renovation and reburhbishment of business premises as per stated in the *First Schedule but shall not include the cost as specified under *Second Schedule, which is certified by an external auditor.

Reference: FAQ under P.U.(A) 381

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.