What are the Conditions for Service Tax B2B Exemption?

Published: 2018

Background

Service Tax is a single-stage tax system and there is no input tax credit mechanism available under the service tax regime. Therefore, it is necessary to consider the service tax exemptions for business to business (B2B) transactions in order to avoid tax cascading effect on the provision of taxable services.

(A) B2B Exemption - Local Services

Effective from 1st January 2019 | Service Tax (Person Exempted from Payment of Tax) Order 2018

General Principle

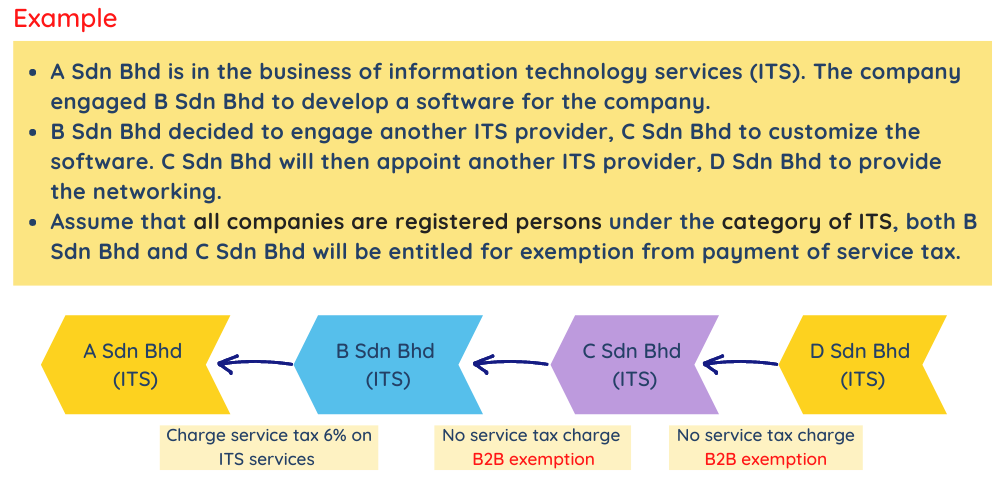

In accordance with the Service Tax (Person Exempted from Payment of Tax) Order 2018, B2B exemption may be eligible to a taxable person who acquires taxable services of the same category from another service tax registered person. The B2B exemption is applicable for the following services:

❖ Professional services (Group G)

❖ Other Service Providers (Group I)

Conditions for B2B exemption

(1) The service recipient and the service provider of taxable service exempted are registered for service tax.

(2) The taxable service exempted is the same service provided by the service recipient (person exempted from service tax payment).

(3) The taxable service exempted is not for the service recipient’s own consumption but for furtherance of business.

(B) B2B Exemption - Imported Services

Effective from 1st January 2020 | Service Tax (Person Exempted from Payment of Tax) Order 2018 Amendment 1/2019 & Service Tax Policy No.2/2020

With effect from 1st January 2020, B2B exemption is expanded to cover the following imported taxable services:

❖ Professional services (Group G)

❖ Other Service Providers (Group I)

Exemption will be given to a registered person who fulfill the following conditions:

(1) Registered person under Service Tax Act 2018 and account for service tax using SST-02 form.

(2) Provide same services to customer as imported taxable services acquired.

(3) Imported taxable service is for furtherance of business and not for personal consumption.

(4) Has paid amount payable for the imported taxable service to the service provider.

(C) B2B Exemption - Issuance of Invoice

Any registered person under the category of B2B exemption, who has provided taxable services to any registered person entitled for the exemption is required to:

i. Issue invoices with the following additional particulars

- Company Name

- Company Address

- SST Registration Number

- Total Amount of Service Charged, and

- Amount of Service Tax Exempted

ii. Ensure that the total amount of service tax exempted due to the B2B exemption is reported in Column 18(c) of Form SST-02 and submitted to the Customs accordingly:

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.