SALES tax

Published: 2018

Effective Date and Scope of Taxation

1 September 2018 (SalesTax)

- Sales Tax is a single-stage tax imposed on taxable goods manufactured locally by a registered manufacturer, and on taxable goods imported by any person.

Section 3 of the Sales Tax Act 2018

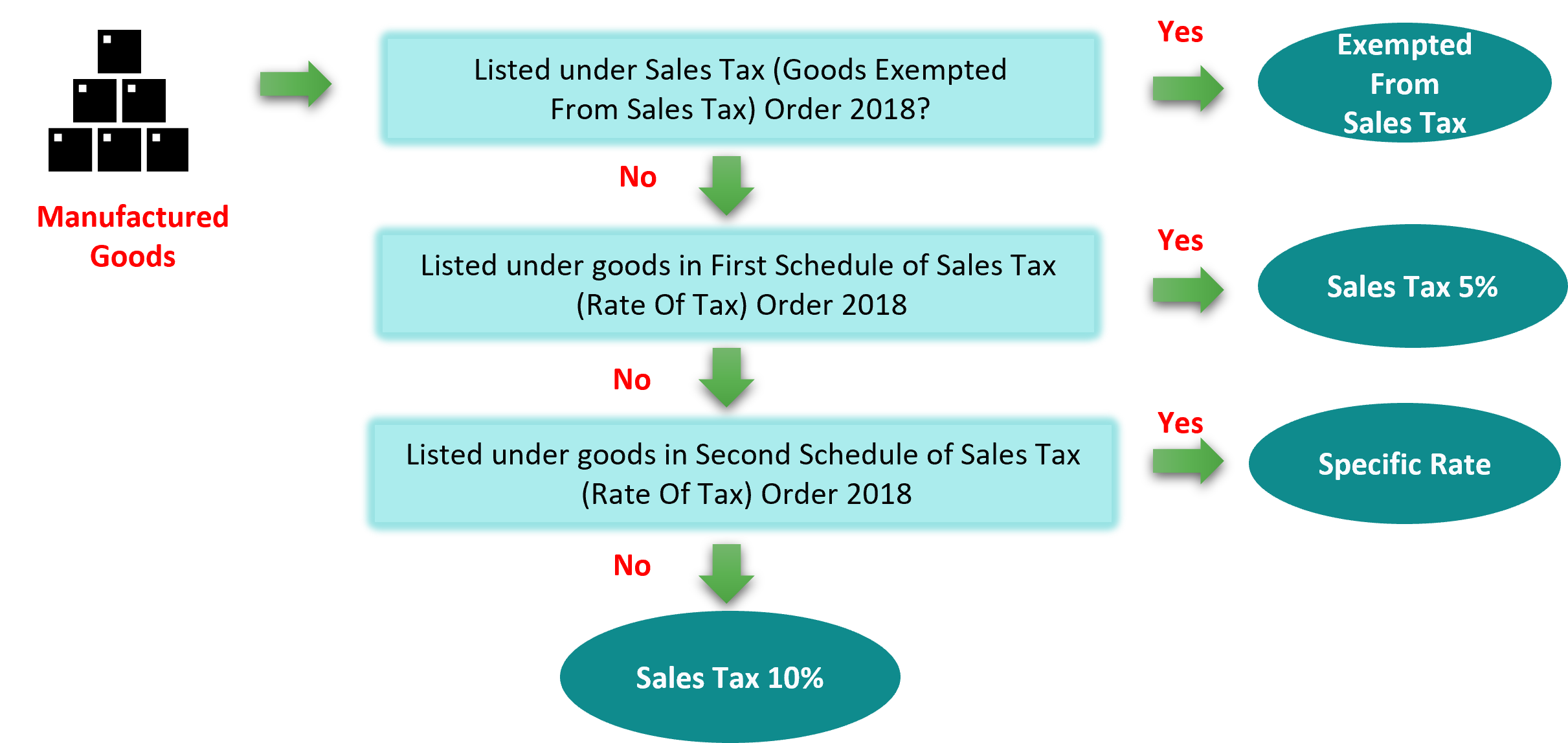

- In relation to goods other than petroleum, the conversion by manual or mechanical means of organic or inorganic materials into a new product by changing the size, shape, composition, nature or quality of such materials and includes the assembly of parts into a piece of machinery or other products, but does not include the installation of machinery or equipment for the purpose of construction; and

- In relation to petroleum, the process of refining that includes the separation, conversion, purification and blending of refinery streams or petrochemical streams.

Rate of Tax

Registration of Taxable Person

Registration

|

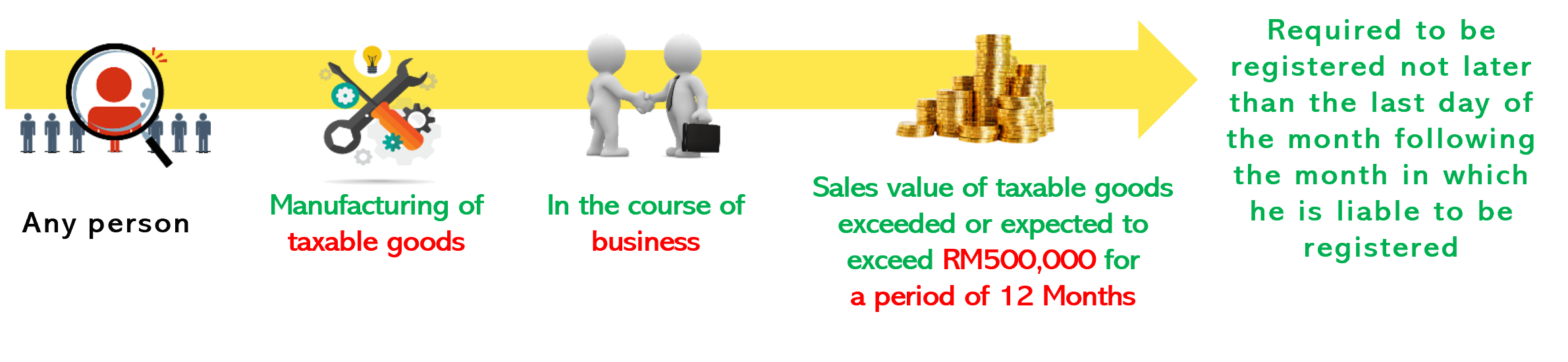

Mandatory Registration A manufacturer is liable to be registered if the total sales value of his taxable goods for a 12- month period exceeds or is expected to exceed RM500,000. |

Voluntary Registration Any manufacturer of taxable goods who is not liable to be registered (below threshold) or exempted from registration (as below) may apply to the Director General (DG) of Customs for registration as a registered manufacturer. |

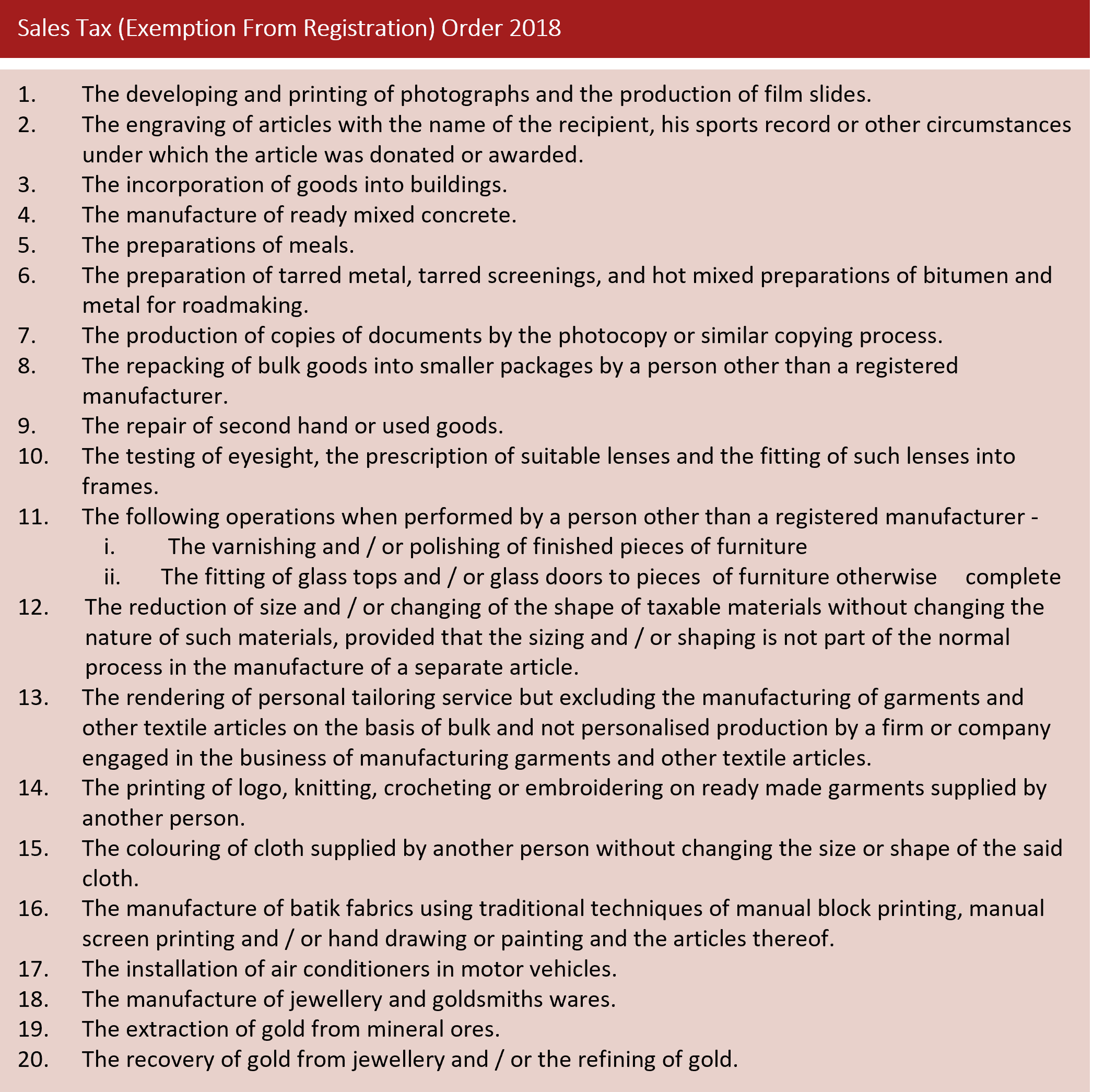

Exemption From Registration

Taxable Period and Sales Tax Due

- Taxable Period

- A taxable period is a period of 2 calendar months, however, a taxable person can apply to the DG of Customs to vary the taxable period.

- The return shall be furnished to the Director General not later than the last day of the month following the end of his taxable period using form SST-02.

2. Sales Tax Due

- Sales tax is due when the taxable goods are sold, disposed of otherwise than by sale, or first used otherwise than as materials in the manufacture of taxable goods.

Offences & Penalties

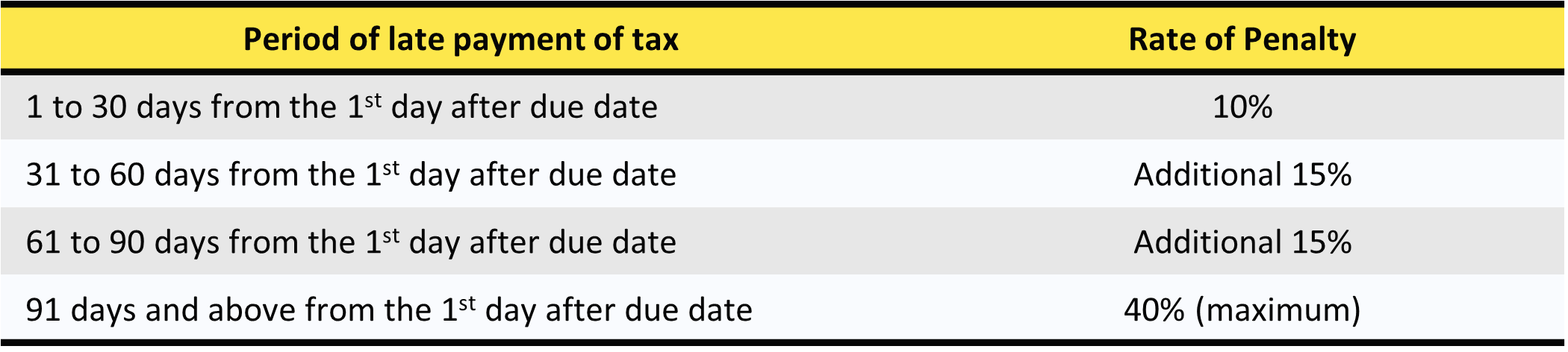

1. Late Payment Penalty

2. Late Submission Of Return

Liable to a fine not exceeding RM50,000 or imprisonment not exceeding 3 years or both under Section 26(7), Sales Tax Act 2018.

Sales Tax Exemption

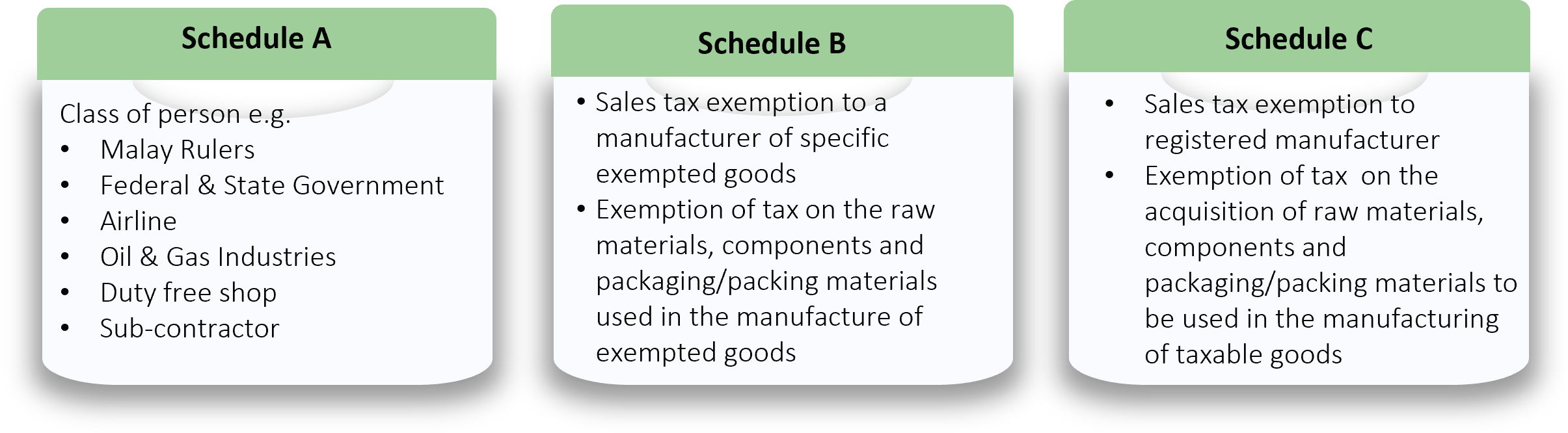

Sales Tax (Persons Exempted From Payment of Tax) Order 2018

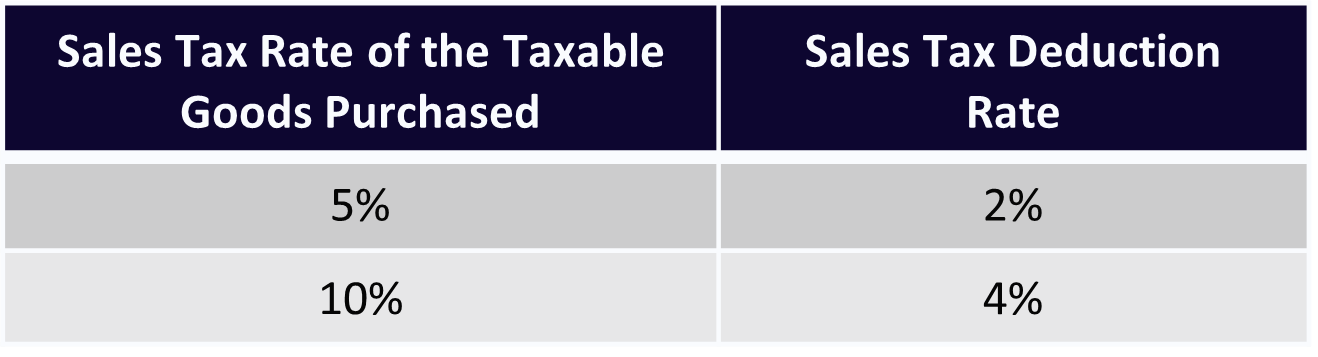

Sales Tax Deduction Facilities

A registered manufacturer may make an application to the Director General for a sales tax deduction in respect of taxable goods (e.g. raw materials, components or packing and packaging materials) purchased from a person other than a registered manufacturer which is used solely in the manufacturing of taxable goods.

This facility is provided to reduce the burden of a registered manufacturer who purchases manufacturing inputs

from a supplier and not from a registered manufacturer. The sales tax deduction in respect of taxable goods

purchased shall be based on the following rates:

Appendix A

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.