Published: 2021

General Principle

Trade

debt which is irrecoverable either wholly or partly are allowed as a deduction

in ascertaining the adjusted income of a business. Trade debt is a debt that

arises from the sales of goods or services and has been included in the gross

income of the business.

Subsection 34(2) of the ITA allows a trade debt which is reasonably estimated

to be irrecoverable either wholly or partly, to be deducted from gross income

in computing the adjusted income of the business.

Where a trade debt is written off as bad or an amount of debt which is

estimated to be irrecoverable has been subsequently received, the total debt

which is recovered shall be regarded as a gross income of the business since

deductions have been made in relation to the debt and such estimates (provision)

1. Irrecoverable Debts (Bad Debts)

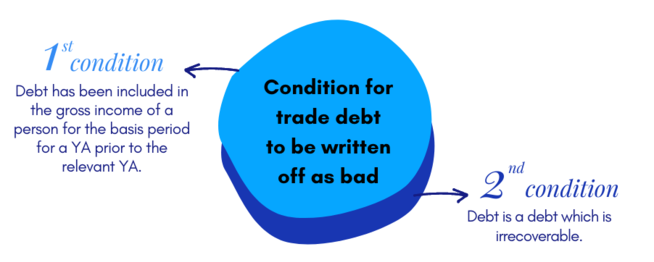

Trade debts which have long not been paid and have been identified as wholly irrecoverable are known as bad debts. Typically bad debts will be written off and claimed as deductions in ascertaining the adjusted income of the business.

Sound considerations as follows should be taken by the person carrying the business before a trade debt can be written off.

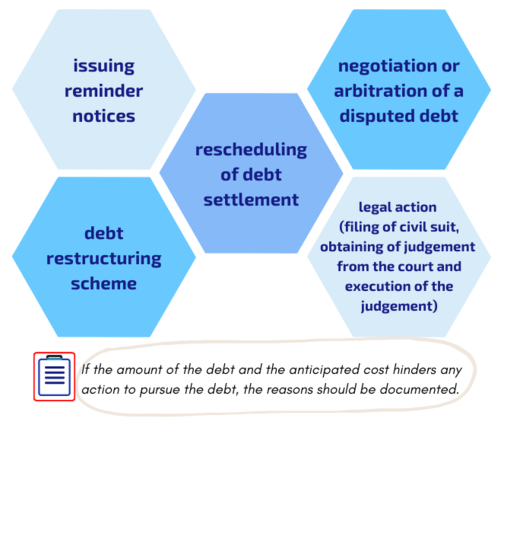

i. Steps taken to recover the debt

Reference: PR No. 4/2019

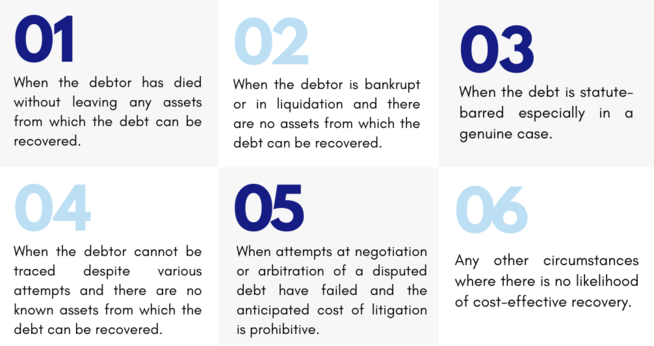

ii. A debt can be considered as bad in the following circumstances:

2. Doubtful debts

Trade

debts which are reasonably estimated to be partly irrecoverable in which the

debt is doubtful to be fully recoverable. It is a trade debt that has not yet

been paid off but has the hope to be partly recovered. (paragraph 34(2)(b) of

the ITA).

Subsection 34(2) of the ITA allows a provision made for trade debts which are

reasonably estimated to be irrecoverable as a deduction in ascertaining the

adjusted income of a business.

Specific provision for doubtful debts

✔ Provision is made at the

end of the accounting period

✔ For debt which is

expected to be irrecoverable & determined with reasonable grounds

✔ Allowed as a deduction

General provision for doubtful debts

✔ Provision is made based

on general information

✔ Not allowed as a

deduction

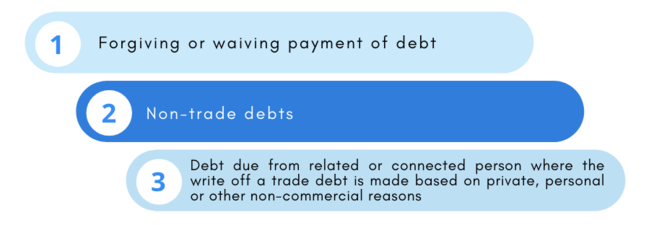

Circumstances Where Irrecoverable Debts Are Not Allowed as Deductions:

Reference: PR No. 4/2019

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.