Can a Company Loan to Its Directors?

Published: 2022

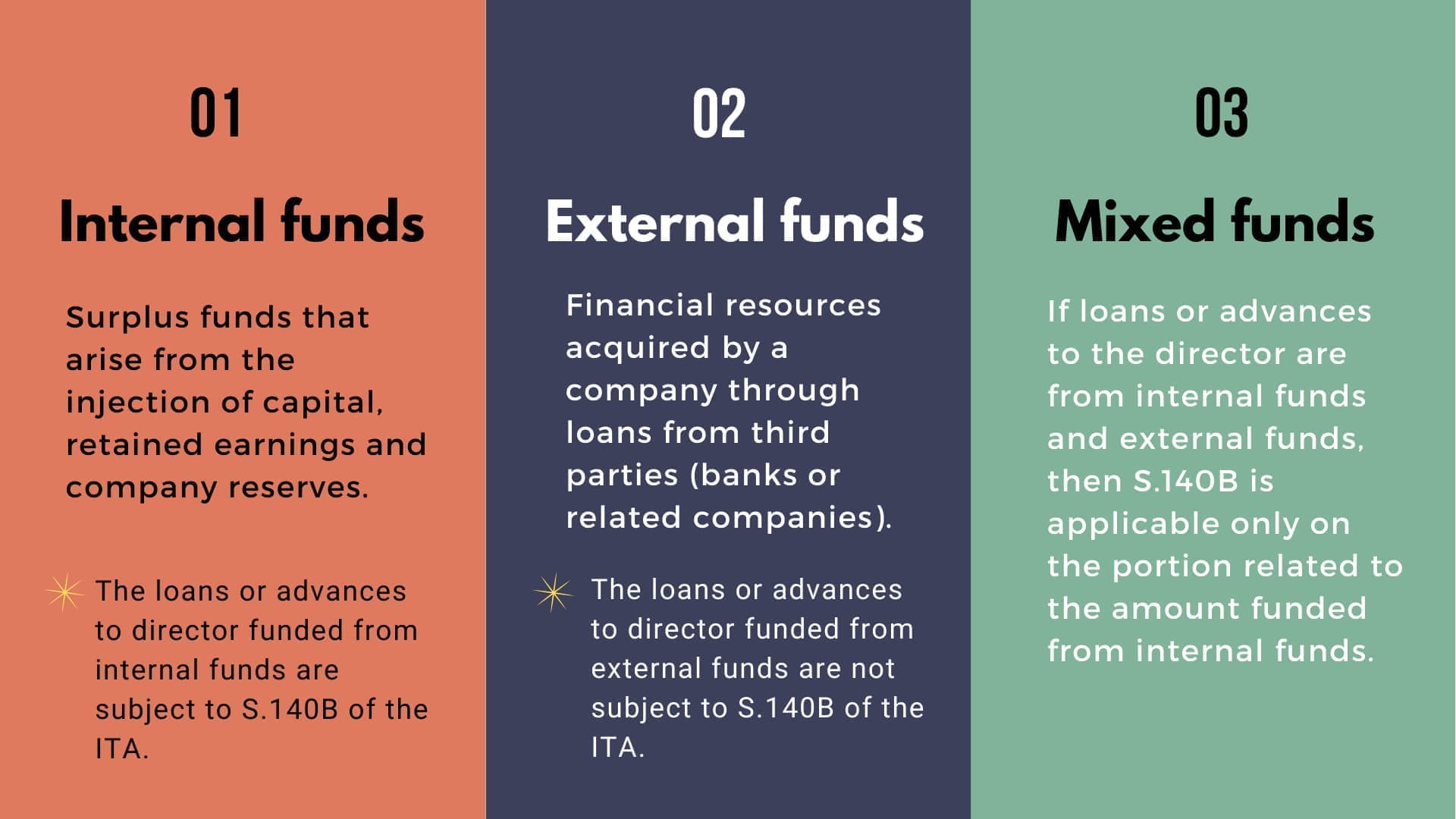

Under S.140B, a company that provides loans or advances to directors, which are funded from internal funds shall be deemed to have a gross income consisting of interest from such loans or advances for that basis period. Such interest is assessed under paragraph 4(c) of the ITA.

However, if the loans or advances to directors are financed from external funds or third party, then the provision of S.140B of the ITA is not applicable.

Funds For Loans Or Advances to Director

Computation of Deemed Interest Income On Loan

Or Advances To Directors of The Company

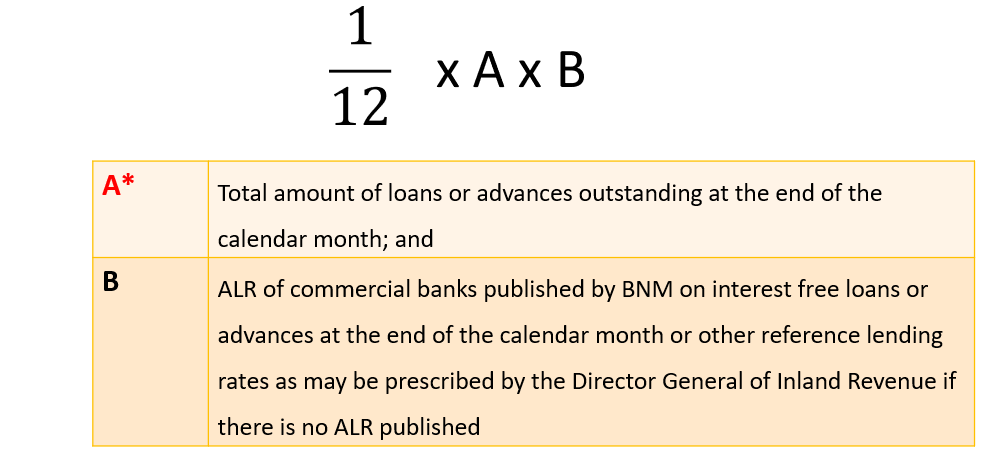

The sum of the monthly interest is determined in accordance with the formula:

*A = balance of loans or advances after deducting repayment of loans or advances and adding any new loans or advances made during that month.

Determination On The Amount Of Interest Income Deemed To Be Received By The Company

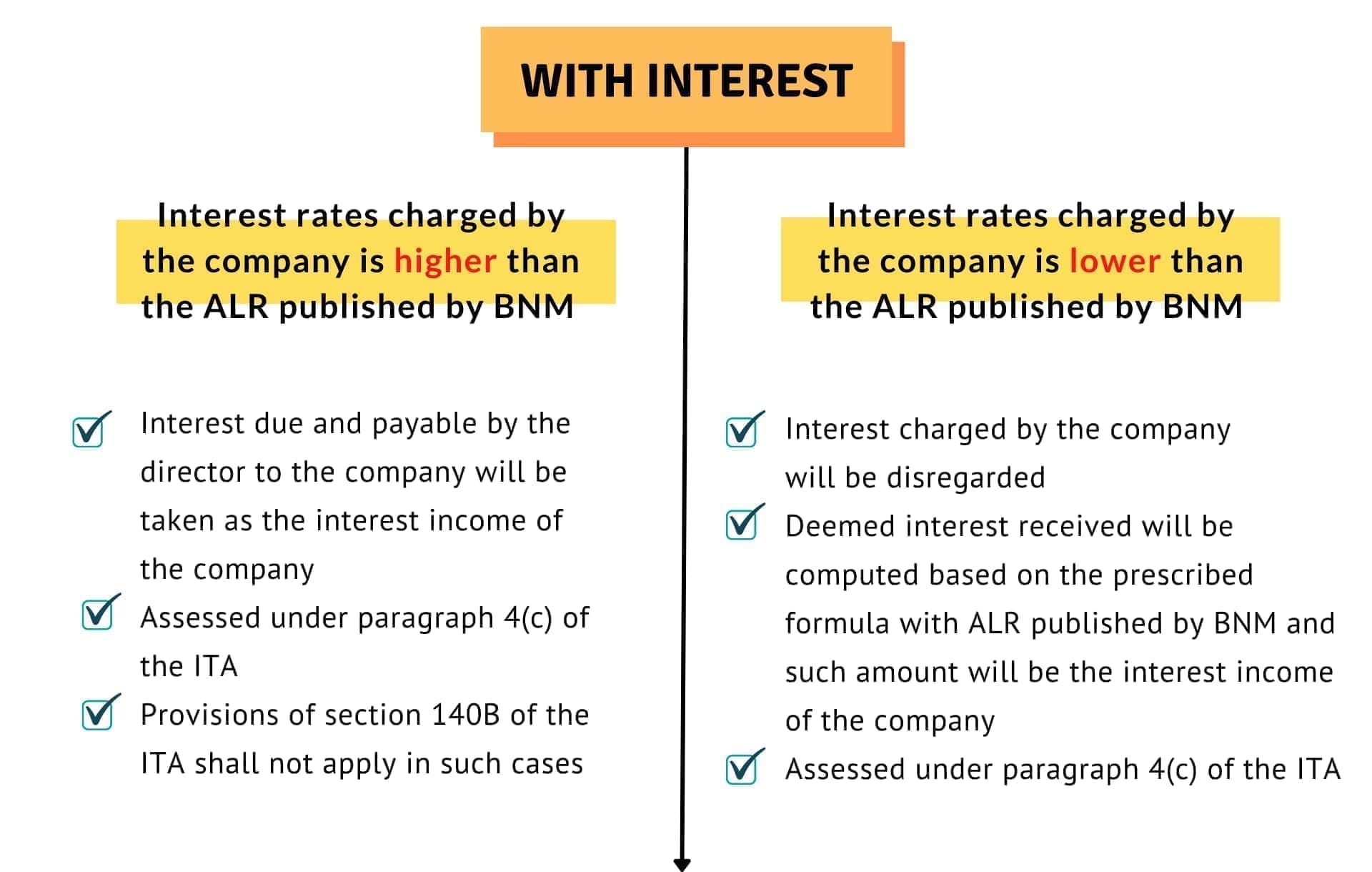

Interest-free: The amount of interest will be computed or determined based on the prescribed formula with ALR published by BNM in the basis year in which the loans or advances are given.

Other Provisions Related To Loan Or Advances To Directors

Loan to Directors by a Dormant Company

👉Company deemed to commence operations

👉Loans to directors are subject to S.140B

👉Interest deemed to be assessed under paragraph 4(c)

Loans or advances to directors via a partnership

👉 Loans by a company to a partnership in which the partners are also directors are subject to S.140B

👉Total loans made to directors are based on the percentage of capital contribution of each partner

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.