Published: 2021

A. Service Tax on Imported Taxable Services

With effect from 1st January 2019, taxable service acquired by any person in Malaysia from any person who is outside Malaysia for the purpose of business will be subject to 6% imported service tax. This will include taxable services acquired by person not registered under sales and service tax.

Type of Imported Taxable Services Subject to Service Tax

Taxable Imported services shall be the taxable services as prescribed under First Schedule of Service Tax Regulation 2018. Generally, this would include professional services such as legal services, IT services, digital services, engineering services, architectural services, management services etc. The service tax is to be borne by the payer of the fees for such services.

Businesses that have been charged service tax on imported digital services by Foreign Registered Person is not required to account for service tax on the same imported taxable services. Please refer to Part B of this article for further explanation on digital services acquired from foreign registered person.

Service Tax Due

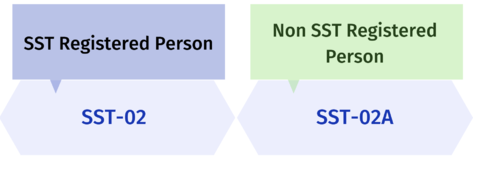

Service tax on imported taxable services will be due at the time when the payment is made or invoice is received for the service, whichever is the earlier. Payer who is a registered person is required to self-account for the 6% service tax and declare in the SST-02 return in accordance to existing taxable period.

Where any person who is not a taxable person but carries on a business acquires any imported taxable service, a service tax declaration and payment of the service tax must be made to the Direct General via a specific SST-02A return by the last day of the month following the end of the month in which the payment for the imported service has been made by him or the invoice for such services has been received by him (whichever is earlier).

Service Tax Exemption

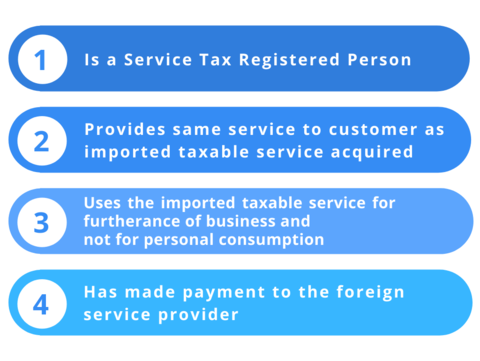

Effective 1st January 2020, registered person is granted exemption by the Minister to account and pay service tax on imported taxable services.

The exemption is subject to the conditions that the service acquirer:

Imported taxable services eligible for the above exemption are as follows:

Professional services under Group G (except employment and private agency services)Advertising services under item 8, Group I, First Schedule of the Service Tax Regulations 2018

Penalty for Non-Compliance

Any person who fails to comply with the above requirement shall, on conviction, be liable to a fine not exceeding thirty thousand ringgit or to imprisonment for a term not exceeding two years or to both.

Reference:

Service tax Act 2018Service Tax Policy No 2/2020

B. Digital Services Acquired from Foreign Registered Person (FRP)

With effect from 1st January 2020, local businesses are not required to self-account for the 6% service tax on the imported digital services acquired from foreign registered persons. The reason is that the foreign registered person will impose a 6% service tax on the digital service rendered to the consumer in Malaysia.

Want to know how to claim refund on digital tax paid to foreign registered person (FRP)?

Click the button below to read more about the subjected conditions and method for claiming refund on digital tax paid to foreign registered person (FRP).

Home About Us Contact Us Site Map

Copyright 2026 YYC HOLDINGS SDN BHD 201501018259 (1143591-H) All rights reserved.